Modern Mone(tar)y Theory

Assets and Liabilities net to zero, Stocks and flows, What is money?

A growing theory in the field of economics is Modern Monetary Theory(MMT). The essence is that a government issuing its own currency does not have any budgetary constraints. In a dynamic with the central bank, the government can “finance” deficits by selling government bonds to the central bank. The government does not need taxes to finance its spending, but taxes create demand for the money and function as a control tool to avoid inflation.

Assets and Liabilities net to zero

An understanding of the MMT-approach starts with a basic understanding of accounting. In very simple terms: One’s financial asset is another’s financial liability. Every financial asset(house, savings account) is negated by a corresponding financial liability(mortgage, a bank’s liability).

The net financial wealth can be calculated as the sum of all financial assets minus the sum of all financial liabilities. This can be explained by looking at a household. If the savings in the bank and the value of the house is higher than the debts, the net financial wealth is positive. Reversely, if it is lower, the net financial wealth is negative.

Let us assume the economy only consists of households. For one household to have a net financial wealth that is positive, another household needs to offset this with a net financial wealth that is negative. Assets and liabilities need to balance each other, and the net financial wealth of all the households has to be zero.

For the net financial wealth of all the households to be different than zero, there needs to be another actor in the economy. If we add a government it is possible that the government has a net financial wealth that is negative, so that the net financial wealth of the households can be positive.

In the real economy, it makes sense to make a division between the private sector(consisting of households and firms), the government, and foreign exchange. We, then, end up with the equation for net financial wealth:

Domestic Private Balance + Domestic Government Balance + Foreign Balance = 0

Stocks and flows

Assets and Liabilities represent the economy through the lense of stocks. Stocks describe sizes, where one's financial asset is another's liability. Stocks can be seen as a screenshot of the economy at a moment in time. But if we take a new screenshot some time later, we will see that some of the stocks have changed. What has happened in between, and what is continuously happening, is a flow of money.

The stocks and flow are dependent on each other. Mathematically, integrating the flow over time gives us the stocks, and, practically, the distribution of stocks influences flows of money. This is a simplification that makes sense if the accumulation of wealth is in money. If the accumulation of wealth was in the stock market instead, the integration of flows would not necessarily hold true since the stock market can be priced at multiples that are higher than the underlying liquidity.

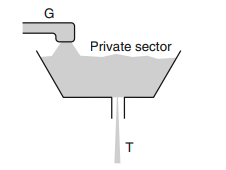

Accumulation of wealth in the form of money at the individual level would then necessitate a positive flow of money over time, achieved by spending less than one's income. This can be explained with a bathtub analogy, where there is water flowing in representing the income, there is water flowing out representing the spending, and the difference between these two over time determine the water level, which is the accumulation of wealth. Note here that this analogy does not extend into the negative domain.

This analogy can also explain the relationship between the government and the private sector. Here, the water level represents the net financial wealth in the private sector, the flow in is government spending on goods and services, and the drain is government taxes.

From this we get the first part of the well-known accounting identity:

S ≡ (G – T),

where S is the savings in the private sector, G is government spending on goods and services, and T is taxes. G-T is the government deficit, and from the accounting identity this cannot be different from the Savings. In reality, the economy also consists of firms and a foreign sector so that the private savings is also a product of investments and net exports. The main point, however, is to illustrate the relationship between government deficit and private saving.

What is money?

The previous analogy implies that government spending is independent of government taxes. This stands in contrast to the view where the government budget is financed by taxes, and the government needs to collect taxes before it can spend. To explain why this is not the case we have to understand what money truly is.

“All “modern money” systems (including those of the “past 4000 years at least” as Keynes put it) are state money systems in which the sovereign chooses a money of account and then imposes tax liabilities in that unit. It can then issue currency used to pay taxes” (Wray)

Let's use the US Dollar as an example. The US Dollar is a fiat currency, meaning that the currency is not backed by gold. The currency - a government IOU - has no guaranteed convertibility, but the government promises to accept it in payments to itself through taxes. The taxes create the demand for the IOUs and drive the money. But, in order to pay taxes, the population first has to obtain the IOUs through government spending. Spending needs to happen before taxes can be collected.

When the government spends more than it collects in taxes, it needs to fill this gap by selling government bonds. These bonds can be bought by banks, foreigners or investors. And in the absence of any buyers, the Central Bank can buy the bonds by creating new reserves:

“The United States can pay any debt it has because we can always print money to do that. So there is zero probability of default” (Greenspan)

This means that a government with its own fiat currency cannot default on its debt as long as it is denominated in its own currency. The government is unconstrained in its nominal spending power, but limited by real resources and inflation. But although the government can spend, it does not mean it should.

Erlend